.png)

payment charges

What Are Payment Charges?

Payment charges are fees assessed at each stage of a transaction, from the card network to the processor to your bank. Businesses that accept digital payments absorb these costs, often without a clear picture of what each fee covers.

Key Insight: Payment charges are not a single fee. They are layered, and understanding each layer is the first step toward controlling costs.

The three core components are interchange fees (paid to the card-issuing bank), assessment fees (paid to card networks such as Visa or Mastercard), and processor markup (your payment provider's margin). Together, they typically total 1.5% to 3.5% per transaction for card payments.

Minimize Fees with Smart Collections

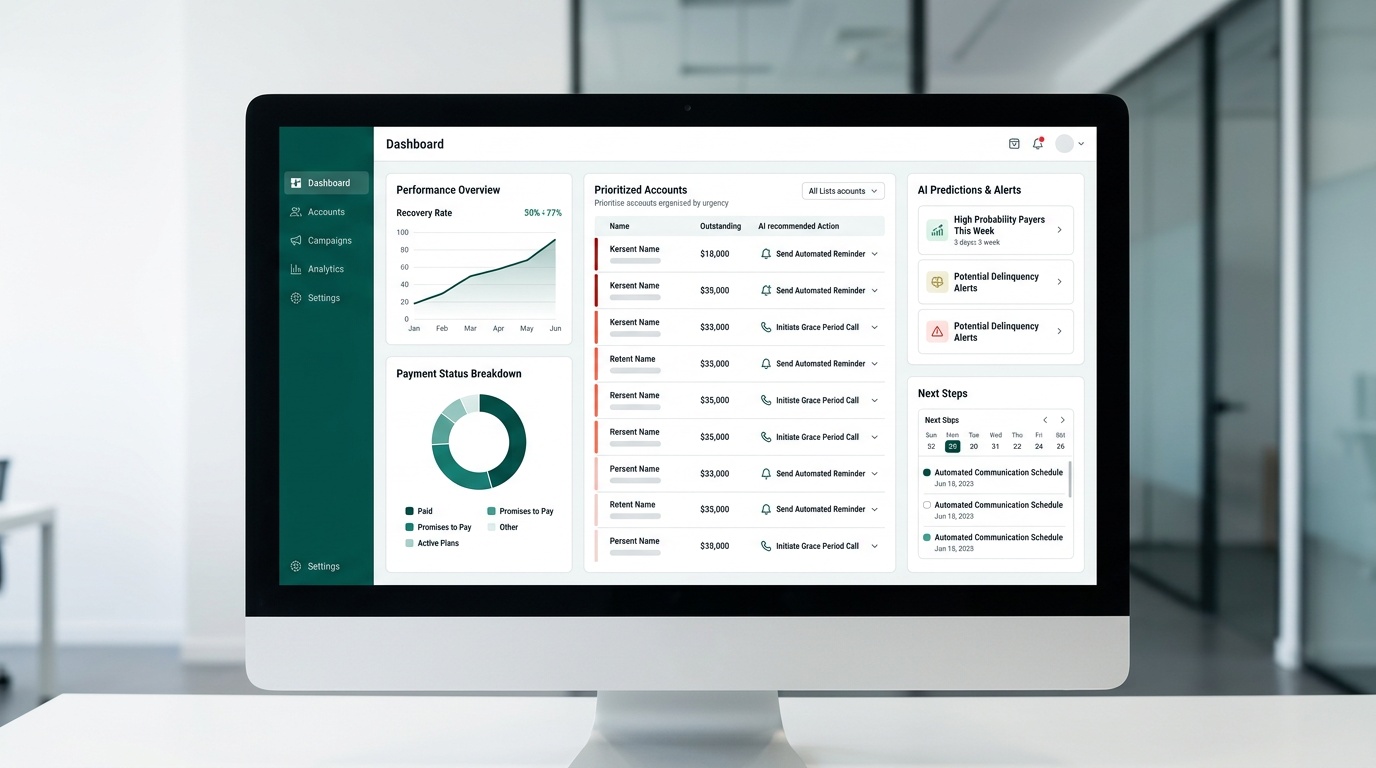

Overdue receivables increase fee exposure. Each failed attempt, retry, and chargeback adds cost. Faster recovery reduces retries and disputes.

Dash automates outreach by text and email, routes customers to self-service payment tools, and supports configurable payment plans. Teams using Dash report increases in payments collected and payment schedules established.

Dash uses a fixed monthly platform fee with no commissions on recovered amounts. That pricing removes the percentage-based drain common to third-party collections and keeps overhead predictable.

Reclaim control of receivables. See how Dash works and cut collection costs.

Common Types of Fees and How They Add Up

Fees add up across categories, and each one reduces margin in a different way. Identify which fees apply to your payment methods and customer mix.

| Fee Type | Who Collects It | Typical Range |

|---|---|---|

| Interchange Fee | Card-issuing bank | 1.15%–2.40% |

| Assessment Fee | Card network (Visa, Mastercard) | 0.13%–0.15% |

| Processor Markup | Payment processor | 0.20%–0.50%+ |

| Chargeback Fee | Processor or acquiring bank | $15–$100 per dispute |

| ACH Transfer Fee | Payment processor | $0.25–$1.50 flat |

Healthcare and property management teams can face higher exposure when late payments trigger retries, disputes, and processor penalties. ACH is often the lowest-cost option for recurring balances, especially when billing is predictable.

Payment Charges vs. Traditional Collections: A Cost Comparison

Payment charges are a processing cost. Traditional collections are a revenue-recovery cost. Each requires a different approach and has a different impact on margins and customer experience.

| Cost Factor | Standard Payment Processing | Traditional Collections | Dash Fixed-Fee Model |

|---|---|---|---|

| Fee Structure | Per-transaction percentage | 25%–40% commission on recovered amounts | Fixed monthly platform fee |

| Predictability | Variable by volume | Unpredictable, scales with recovery | Predictable overhead |

| Customer Relationship | Neutral | Often damaged by third-party contact | Supported through self-service tools |

| Compliance Risk | Low | High without careful oversight | Built-in FDCPA, TCPA, and HIPAA guardrails |

| Recovery Speed | Immediate on successful payment | Weeks to months | Teams report results within the first week |

Third-party collections can take a large share of recovered revenue before it reaches your business. A 30% commission on a $10,000 recovered balance costs $3,000. Dash replaces commission pricing with a fixed monthly fee, so more recovered revenue stays with your business.

✅ Pros of Dash's Fixed-Fee Model

- Predictable monthly cost regardless of recovery volume

- No commission deducted from recovered balances

- Compliance guardrails reduce regulatory exposure

❌ Cons of Commission-Based Collections

- 25%–40% of recovered revenue surrendered per account

- Customer relationships frequently damaged by third-party contact

- Compliance risk increases without direct oversight of outreach

Reducing payment charges starts before a transaction fails. Faster recovery means fewer retries, fewer chargebacks, and fewer processor penalties. See how Dash works to keep more recovered revenue with your business.

The payment processor markup is a component of overall costs that businesses often overlook; understanding the latest interchange fees can help in formulating better financial strategies.

However, regulatory frameworks also play a crucial role in determining fee structures, and the interchange fee standards established by authorities like the Consumer Financial Protection Bureau help shape these rules.

For those seeking deeper insights into the fee mechanisms and their various implications, the Interchange fee article offers a comprehensive overview and contextual background.

Frequently Asked Questions

What are payment charges?

Payment charges are the various fees businesses incur at each step of a digital transaction, from the card network to the payment processor and the bank. These are not a single, flat fee but rather a layered cost that businesses absorb when accepting digital payments. Understanding these layers is key to managing your operational expenses effectively.

What types of fees make up payment charges?

Payment charges are typically composed of three main types: interchange fees, paid to the card-issuing bank; assessment fees, paid to card networks like Visa or Mastercard; and processor markup, which is your payment provider's margin. Other fees, such as chargeback fees for disputes or flat ACH transfer fees, can also contribute to overall costs.

Is a 3% transaction fee considered high for card payments?

A 3% transaction fee falls within the typical range for card payments, which generally total between 1.5% and 3.5% per transaction. While it's not unusually high, it represents a significant portion of your revenue per transaction. Businesses should review their fee structures to ensure they are getting competitive rates.

Is it legal for businesses to charge a 3% fee on debit card transactions?

The legality of charging customers a percentage fee on debit card transactions can vary significantly based on card network rules and state regulations. While credit card surcharging is permitted in many places with proper disclosure, debit card surcharging is often more restricted or prohibited. Businesses should consult their payment processor and legal counsel to understand applicable rules.

How do payment charges differ from traditional collection costs?

Payment charges are primarily processing costs incurred during a transaction, whereas traditional collection costs are expenses associated with recovering overdue revenue. Payment charges are typically a per-transaction percentage, while traditional collections often involve high commission fees on recovered amounts. This distinction means they impact your margins and customer relationships in different ways.

How can businesses minimize the costs associated with payment charges and collections?

Minimizing payment charges begins with understanding each fee component and optimizing your payment methods. For collections, faster recovery of overdue receivables is key, as failed attempts and chargebacks add significant costs. Solutions like Dash help by automating outreach, routing customers to self-service payment tools, and supporting configurable payment plans, replacing commission-based collection fees with a predictable fixed monthly platform fee.