in-house collections vs third-party agencies which is better

Pros and Cons of Each Collections Approach

Choosing between in-house collections and third-party agencies requires weighing trade-offs in cost, control, and customer impact. Here's what each approach delivers--and where each falls short.

Quick Answer: For most businesses, in-house collections win for early-stage accounts when you pair them with automation and clear compliance processes. Third-party agencies make sense for late-stage accounts after internal efforts stop producing payments.

In-House Collections

Pros

- You own the entire customer experience--messaging, timing, and tone stay on-brand

- Lower cost per dollar recovered (no 25% to 50% commission drain)

- Direct access to customer data and payment history for faster resolution

- Protects brand reputation and preserves customer relationships

- Real-time visibility into recovery performance and metrics

Cons

- Requires staff time and training to execute well

- Compliance monitoring demands ongoing attention

- Manual processes limit scalability without automation

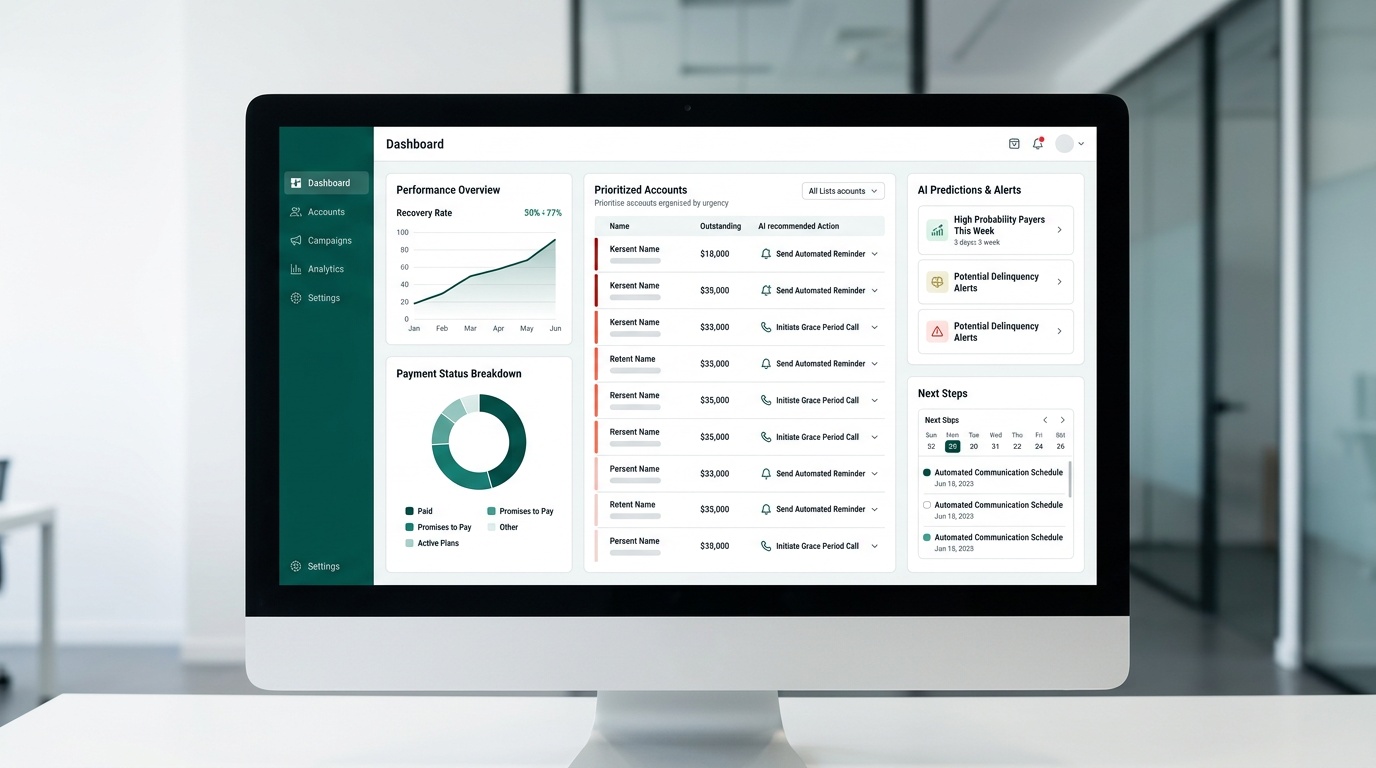

Dash eliminates the operational burden by automating workflows, applying compliance guardrails, and enabling payment plans with minimal setup. Your team stays in control while the platform handles the heavy lifting.

Third-Party Agencies

Pros

- Offloads collections workload from internal teams

- Brings specialized experience with difficult or aged accounts

- Contingency fees mean you pay only on successful recovery

Cons

- Commission rates (25% to 50%) significantly reduce net recovery

- You lose oversight of customer interactions and brand messaging

- Reputation risk from aggressive tactics you can't monitor

- Customer data security and privacy concerns from third-party access

- Limited transparency into collection activity and methods

In-House Collections vs Third-Party Agencies: Side-by-Side Comparison

This comparison clarifies where each approach excels and where it creates operational friction.

| Criteria | In-House Collections | Third-Party Agencies |

|---|---|---|

| Cost Structure | Fixed platform fees or salary costs; no commissions | 25% to 50% commission on recovered amounts |

| Control and Customization | Complete authority over messaging, payment plans, and timing | Limited input; the agency dictates the approach and communication style |

| Customer Relationship Impact | Maintains relationships through respectful, branded outreach | Higher risk of relationship damage from aggressive tactics |

| Compliance Management | Direct oversight with built-in guardrails (FDCPA, TCPA, and HIPAA, as applicable) | Dependent on agency practices with minimal visibility |

| Data Security | Customer data stays internal; SOC 2-certified platforms available | Data sharing with a third party increases security exposure |

| Recovery Speed | Immediate action on overdue accounts without handoff delays | Delays occur during transfer and onboarding |

| Transparency and Reporting | Real-time dashboards and audit logs | Periodic reports with limited operational detail |

For early-stage delinquency, first-party outreach delivers stronger outcomes. See InsideARM for industry benchmarks and perspectives on recovery rates.

Why In-House Collections Win with Modern Automation

When evaluating in-house collections vs third-party agencies which is better, the answer hinges on three factors: control, cost, and customer experience. In-house wins on all three when you deploy the right automation.

Dash delivers AI-powered outreach, configurable payment plans, and compliance workflows that keep your team consistent. You set the tone and timing. Dash handles task routing, messaging sequences, and reporting.

The math is straightforward. A $10,000 recovery through an agency nets you $5,000 to $7,500 after commissions. The same recovery in-house retains the full amount minus internal costs--typically a fraction of agency fees.

You also eliminate handoff delays. Accounts stay in your system from day one of delinquency, so outreach begins immediately instead of waiting for agency onboarding.

Request a demo to see how Dash supports first-party collections and helps you reduce reliance on outside agencies.

When to Choose In-House Collections

In-house collections outperform third-party placements for accounts under 90 days overdue. You maintain direct communication, offer flexible payment options, and keep 100% of recovered funds.

Third-party agencies earn their commission on severely delinquent accounts--typically 180+ days overdue--when escalation requires outside specialization or when internal efforts have stopped producing payments.

The decision isn't binary. Many businesses run a hybrid model: first-party outreach for early delinquency, agency placement for aged accounts. This maximizes recovery while protecting customer relationships during the critical early stages.

Future-Proofing Your Collections Strategy

Regulatory scrutiny isn't easing. The Consumer Financial Protection Bureau expanded FDCPA coverage in 2021, and state rules continue adding requirements. First-party operations give you direct oversight of scripts, contact policies, and dispute handling--oversight you can't replicate with outsourced placements.

Automation supports this oversight by standardizing outreach, improving segmentation, and enabling earlier risk detection. When your team owns the process, you control compliance from start to finish.

If you want a system built for first-party workflows, see how Dash works. The platform handles FDCPA contact limits, TCPA consent verification, and audit trail generation automatically.

When deciding in-house collections vs third-party agencies which is better, start with account age, internal capacity, compliance needs, and the customer experience you need to protect. For most businesses with receivables under 90 days overdue, in-house wins--especially when backed by automation that eliminates manual overhead.

The transparency differences between first-party and third-party collections also explain why many companies prefer maintaining operational control.

With compliance management becoming increasingly complex, direct oversight has shifted from optional to essential for businesses that want to avoid regulatory penalties and maintain customer trust.

Frequently Asked Questions

What is the main difference between in-house collections and third-party collections?

The main difference lies in who manages the overdue accounts and the associated control and costs. In-house collections mean your own team handles outreach, giving you full control over messaging, customer experience, and data. Third-party agencies take over the collection process, often charging commissions but reducing your internal workload, with less control over their methods.

When is it better for a business to use in-house collections versus a third-party agency?

For most businesses, in-house collections work best for early-stage accounts, typically under 90 days overdue, especially when supported by automation. This approach helps maintain customer relationships and avoids high commission fees. Third-party agencies are often better suited for severely delinquent accounts, like those 180+ days overdue, or when specialized escalation is needed after internal efforts stop producing payments.

Why do businesses offer payment plans for overdue accounts?

Offering flexible payment plans for overdue accounts, especially through in-house collections, can help customers manage their debt more effectively. This approach supports customer relationships and can lead to higher recovery rates by making payments more accessible. It also allows businesses to retain more of the recovered amount compared to agency commissions.

What are the benefits of managing collections in-house?

Managing collections in-house offers complete control over customer interactions, messaging, and timing, which protects your brand reputation. It also results in a lower cost per dollar recovered because you avoid commission fees, and provides direct access to customer data and real-time performance visibility. This approach supports customer relationships through respectful outreach.

What are the potential risks of using third-party collection agencies?

Using third-party agencies can introduce risks such as less control over customer interactions and brand messaging, potentially damaging customer relationships through aggressive tactics. There are also concerns about customer data security and privacy, as well as limited transparency into their collection activity. High commission rates, typically 25% to 50%, also reduce your net recovery.

How can automation help a business with in-house collections?

Automation can significantly reduce the operational burden of in-house collections by streamlining workflows and applying compliance guardrails. Tools like Dash help teams recover overdue accounts faster using AI-powered outreach and self-service tools. This allows your team to stay in charge of tone and timing while improving consistency and efficiency with fast and easy setup.

Why is compliance management important for collections?

Compliance management is critical in collections due to high regulatory scrutiny from bodies like the Consumer Financial Protection Bureau. Direct oversight of scripts, contact policies, and dispute handling ensures adherence to regulations like FDCPA, TCPA, and HIPAA, as applicable. In-house operations provide more direct control over these processes than outsourced placements, reducing risk.

.png)