.png)

electronic payments processing

Electronic Payments Processing: The Complete Guide for Modern Businesses

Overdue invoices drain cash flow. Manual follow-up burns staff hours. And the longer a payment sits unpaid, the harder it is to recover. For businesses across financial services, healthcare, property management, and beyond, electronic payments processing has become the operational backbone that separates teams that stay ahead of their receivables from those that fall behind them.

This isn't just about accepting credit cards. Electronic payment services span ACH transfers, wire systems, card rails, and the compliance infrastructure holding all of it together. Get the foundation right and you're not just processing transactions -- you're protecting cash flow, reducing overhead, and giving your team real-time control over every dollar owed.

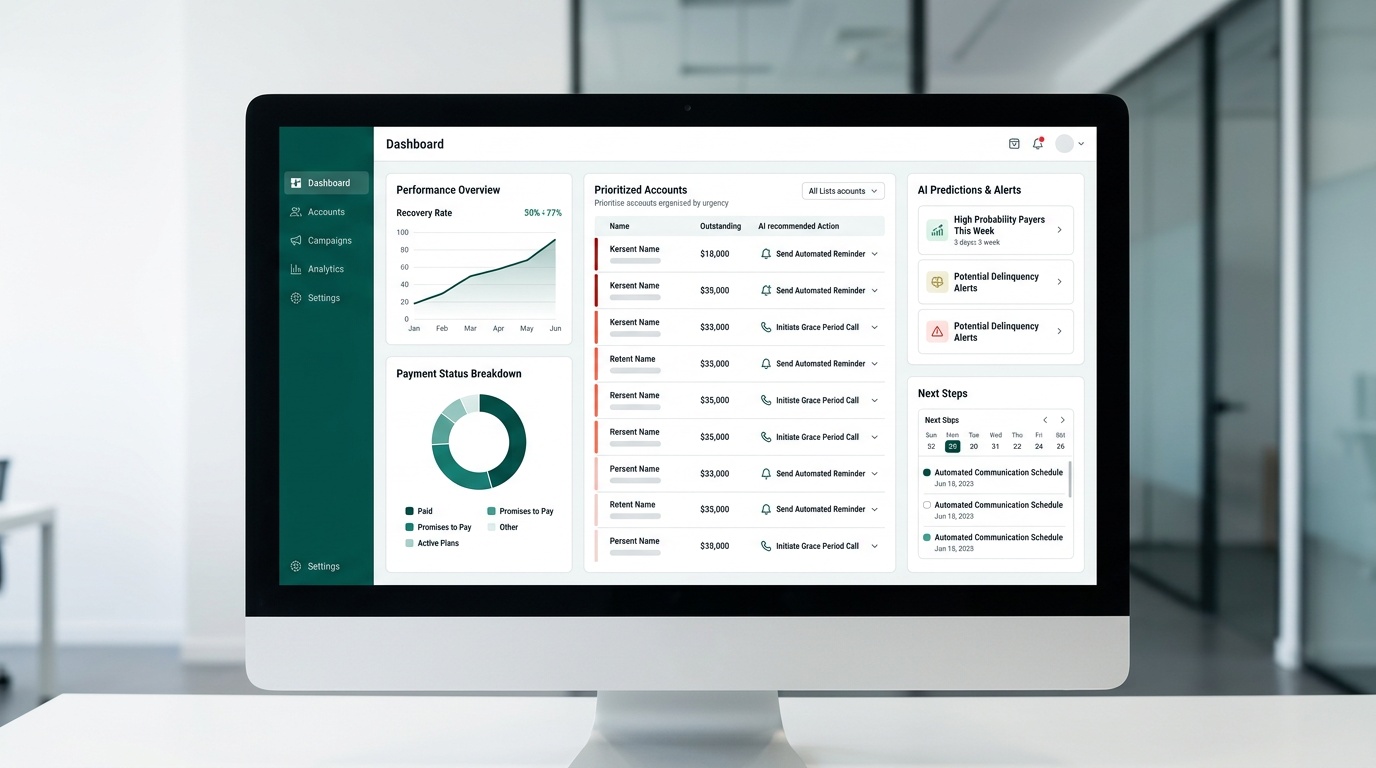

This guide covers what electronic payments processing actually is, why it matters to your bottom line, how to evaluate providers intelligently, and how platforms like Dash connect payment infrastructure to overdue account management so nothing falls through the cracks.

Key Takeaways

- Electronic payments processing replaces paper-based methods with digital fund transfers across ACH, card, and wire networks -- settling faster and with a complete audit trail.

- PCI DSS compliance, fee transparency, and integration depth are the three criteria that separate capable payment providers from costly ones.

- Businesses that pair electronic payment services with receivables management recover overdue balances faster and with less manual effort.

- Dash connects payment workflows directly to overdue account management, so your team tracks, follows up, and recovers -- without outsourcing a single step.

What Is Electronic Payments Processing?

Electronic payments processing is the digital transfer of funds between a payer and a payee through networks such as ACH, credit card rails, or wire systems. No paper. No manual handling. Transactions settle faster, with complete digital records attached.

Businesses across financial services, healthcare, property management, and legal sectors rely on electronic payment services to collect revenue, manage overdue accounts, and maintain cash flow. According to the Federal Reserve, non-cash payments in the U.S. continue to grow year over year, with ACH and card payments leading commercial activity. That growth isn't coincidental -- it reflects a real operational shift toward systems that move faster and cost less than paper-based alternatives.

Each payment method serves a different use case. ACH transfers work well for recurring billing and high-volume B2B payments. Card rails handle point-of-sale and online consumer transactions. Wire systems are used for high-value transfers where same-day finality matters. Understanding which rail fits your workflow is the first step toward building a payment infrastructure that actually supports your business model -- not just one that technically accepts money.

For businesses carrying overdue accounts, the underlying payment infrastructure matters even more. If patients, tenants, or clients can't pay through a convenient digital channel, they often don't pay at all. Friction in the payment experience directly translates to friction in your collections rate.

Benefits of Electronic Payments Processing

Switching to electronic payments processing delivers measurable operational gains. These aren't marginal improvements -- for teams managing high volumes of accounts, the difference compounds quickly:

- Faster collections: Payments settle in hours, not days.

- Reduced errors: Automation reduces manual data entry mistakes.

- Lower costs: Processing fees often cost less than paper check handling.

- Real-time visibility: Track each transaction across accounts as it happens.

Speed matters most when managing overdue receivables. The older a balance gets, the harder it is to recover. A 2023 analysis from the National Automated Clearing House Association (Nacha) showed ACH network volume exceeding 30 billion transfers annually -- a figure that reflects how broadly businesses now depend on electronic rails to keep money moving. When your payment infrastructure is slow or opaque, your entire receivables cycle suffers.

Real-time visibility deserves particular attention. Knowing which accounts have paid, which are aging, and which need follow-up -- all from a single dashboard -- changes how a team operates. Instead of chasing spreadsheets, staff act on current data. That shift alone can cut recovery timelines significantly.

Dash Account Receivables Management connects directly with payment workflows, keeping overdue accounts visible and actionable without outsourcing recovery. Your team stays in control of the process -- and the customer relationship -- throughout.

How to Choose Electronic Payment Services

Not every provider offering electronic payment services is built for businesses that also need to manage overdue accounts. Here's what to evaluate before committing:

- PCI DSS compliance: Required for protecting cardholder data. Non-negotiable.

- Fee transparency: Flat-rate or interchange-plus pricing is easier to forecast than tiered pricing, which can obscure your true cost per transaction.

- Integration depth: The system should connect with your accounting and receivables tools without custom development work.

- Receivables support: Choose electronic payment services with overdue account management built in, not bolted on.

Fee structure deserves more attention than most businesses give it. Tiered pricing looks simple upfront but frequently results in higher effective rates than interchange-plus or flat-rate models. Run the numbers on your actual transaction mix before signing a contract. A provider that appears cheaper per transaction may cost significantly more at volume.

Integration depth is where many providers fall short. A payment tool that doesn't talk to your accounting system creates manual reconciliation work. A receivables platform that doesn't surface overdue accounts in your payment workflow creates blind spots. The best setups eliminate both problems -- your team sees what's owed, communicates with the account, and collects through a single connected system.

Dash Account Receivables Management gives businesses a streamlined way to track overdue payments, automate outreach, and keep every step documented -- without the cost or reputational risk of third-party collections. Learn more at payondash.com/how-it-works.

Compliance in Electronic Payments: What Businesses Need to Know

Compliance isn't just a legal checkbox -- it directly affects how you can contact customers about overdue payments, how you store their data, and what happens if something goes wrong. For businesses managing their own receivables, this matters as much as the payment rails themselves.

The key frameworks to understand:

- PCI DSS: Governs how cardholder data is stored, processed, and transmitted. Any provider handling card payments must meet this standard.

- TCPA: Regulates how businesses contact customers by phone or text, including automated outreach. Violations carry significant per-message penalties.

- FDCPA: Sets rules for how businesses communicate with consumers about overdue accounts -- timing, content, frequency.

- HIPAA: Applies to healthcare businesses handling patient information alongside billing data.

Staying compliant across all four frameworks simultaneously is where many businesses either hand off recovery to a third party (losing control of the customer relationship) or expose themselves to regulatory risk by managing it manually. Neither outcome is acceptable.

Dash is built with compliance guardrails across TCPA, FDCPA, HIPAA, and PCI DSS -- not as an add-on, but as core platform architecture. Your team gets the tools to reach customers at the right times, through the right channels, without stepping outside regulatory boundaries. That's a meaningful operational advantage, especially for healthcare organizations, legal firms, and property managers working under multiple overlapping compliance obligations.

Connecting Electronic Payments to Receivables Recovery

Electronic payment infrastructure and receivables management are two sides of the same cash flow equation. Most businesses treat them as separate systems. The ones recovering overdue balances most effectively don't.

Think of it this way: a great payment processor makes it easy to accept money. But if an account goes overdue, that processor has no mechanism for follow-up, no outreach automation, no compliance guardrails for collections communication, and no dashboard showing you which accounts need attention today. You're back to manual work -- spreadsheets, email threads, phone logs -- and the clock keeps running on aging balances.

Pairing electronic payment services with a dedicated receivables platform closes that gap. Overdue accounts trigger automated, compliant outreach. Customers receive payment links they can act on immediately. Your team monitors everything from a single dashboard, with full audit logs and real-time reporting. Recovery happens faster, with less staff time, and without the cost or relationship damage of outsourcing to a third-party agency.

Teams that use Dash report seeing results within the first week of onboarding. The platform supports unlimited accounts, texts, and emails -- no volume caps -- on a fixed monthly fee with no commissions on recovered amounts. For businesses with high account volumes, that pricing model alone changes the math on in-house collections significantly.

Frequently Asked Questions

What is the meaning of electronic payment processing?

Electronic payments processing is the digital transfer of funds between a payer and a payee. It uses networks like ACH, credit card rails, or wire systems to move money without paper. This method results in faster settlements and complete digital records for each transaction.

How long do electronic payments take to process?

Electronic payments typically settle much faster than traditional paper methods, often in hours rather than days. This speed is a significant benefit for businesses, improving cash flow and reducing the wait for funds.

What is an example of electronic payment?

Common examples of electronic payments include transactions made via ACH, credit card rails, and wire transfers. These systems allow for the digital movement of funds, replacing paper checks and manual handling.

What are the main benefits of using electronic payment processing?

Businesses gain several operational advantages from electronic payment processing. These include faster collections, reduced manual errors through automation, and often lower processing costs compared to paper checks. You also get real-time visibility into every transaction.

What should businesses look for when choosing an electronic payment service?

When selecting an electronic payment service, businesses should prioritize PCI DSS compliance to protect cardholder data. Look for transparent fee structures, deep integration with existing accounting tools, and support for managing overdue accounts. This helps ensure your cash flow is protected.

Why is PCI DSS compliance important for payment providers?

PCI DSS compliance is essential because it ensures the protection of cardholder data during transactions. Choosing a compliant provider reduces the risk of data breaches, avoids potential penalties, and safeguards a business's reputation. It should always be a baseline requirement for any payment service.