.png)

FDCPA compliant collections platforms

Overdue receivables are a cash flow problem. A compliance violation is a business risk. When your collections platform fails to enforce the rules of the Fair Debt Collection Practices Act at the system level, you're exposed to both. Choosing an FDCPA compliant collections platform in 2026 is not just an operational decision -- it's a strategic one.

Businesses in healthcare, property management, financial services, and legal sectors face increasing regulatory scrutiny. The CFPB has intensified its supervisory focus on digital collections outreach, and teams relying on manual compliance processes are carrying more exposure than they may realize. A platform that doesn't enforce contact rules automatically, maintain auditable records, and support consumer rights isn't a compliance tool -- it's a liability.

This guide covers what separates genuinely compliant platforms from those that only claim compliance on a marketing page, what features to prioritize during evaluation, and why your pricing model matters more than most businesses expect.

Key Takeaways

- FDCPA compliance must be built into platform architecture, not bolted on as an afterthought.

- Audit logs, contact controls, and opt-out management are baseline requirements -- not premium features.

- First-party collections keep your brand in control while reducing regulatory risk.

- Dash is SOC 2 Type 2 certified and built with FDCPA, TCPA, and HIPAA guardrails natively enforced.

What FDCPA Compliance Requires From a Platform

The FDCPA sets rules on contact timing, frequency, communication content, and consumer rights. Where most businesses get into trouble is assuming their team can manage compliance manually across hundreds of accounts. That assumption breaks down fast. A single missed opt-out, a call placed outside permitted hours, or a communication that omits required disclosures can trigger a complaint, an enforcement action, or worse.

At minimum, any platform you evaluate should include automated contact frequency controls, time zone-aware outreach scheduling, built-in cease-and-desist handling, and complete communication audit trails. These aren't optional enhancements -- they're the baseline. If a platform requires your team to enforce these rules manually, it's shifting compliance risk back onto your staff.

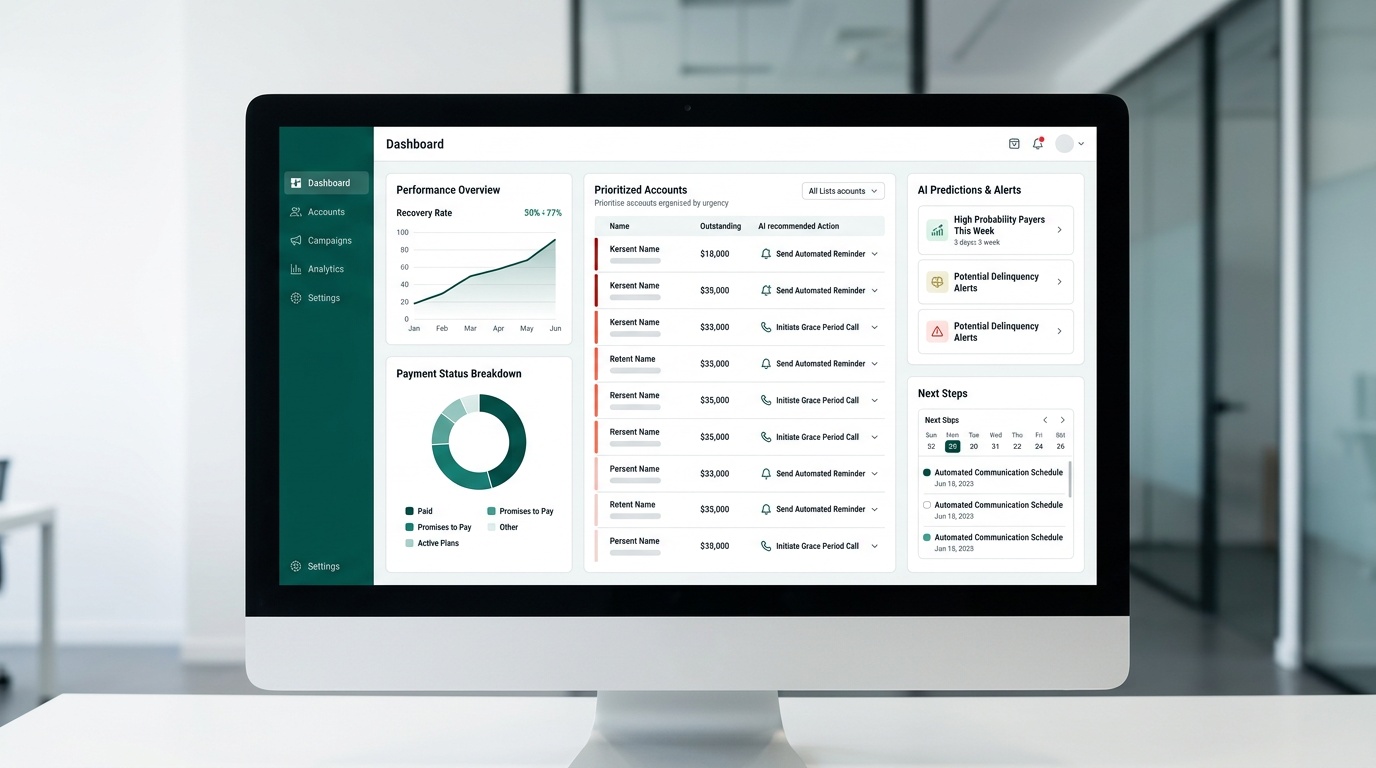

Dash enforces these guardrails natively, so your team doesn't need to manually track compliance thresholds across every account. The rules run at the system level, meaning they apply consistently whether you're managing 50 accounts or 5,000. That consistency is what makes compliance scalable.

It's also worth understanding the regulatory environment around these rules. The CFPB's ongoing supervisory focus on collections practices signals that enforcement pressure isn't easing. Platforms that automate compliance controls now are better positioned for the scrutiny ahead.

Features That Separate Compliant Platforms From Risky Ones

Not all FDCPA compliant collections platforms deliver equal protection. A compliance badge on a pricing page doesn't tell you whether rules are enforced automatically or left to your team to manage. The features below are what separate platforms that reduce risk from those that create it.

- Real-time audit logs: Every outreach attempt, response, and account status change is time-stamped and retrievable. If a dispute arises, you have documentation.

- Opt-out automation: Consumer opt-outs are processed immediately and honored across all channels without manual intervention. No gaps, no delays.

- Configurable outreach rules: Contact windows, message frequency, and escalation paths are configurable by account type -- giving you control without sacrificing compliance.

- SOC 2 Type 2 certification: Independent verification that security and data handling meet enterprise standards. This matters especially for healthcare and financial services clients handling sensitive consumer data.

- First-party workflow support: Your brand communicates directly with customers, preserving relationships and keeping your business in control of tone, timing, and strategy.

Each of these features addresses a specific failure point. Platforms missing even one create gaps that can surface at the worst possible time -- during a dispute, an audit, or a regulatory review. Dash delivers these capabilities in one SOC 2 Type 2 certified platform, built for businesses that want to recover payments while reducing regulatory exposure.

First-party collections deserve particular attention here. When you outsource receivables to a third-party agency, you hand over control of how your customers are contacted -- and how your brand is represented in that interaction. That's a reputational risk as much as a compliance one. First-party outreach keeps the conversation between your business and your customer, which matters for long-term relationships even when the account is overdue.

Pricing Structure and Operational Control

Commission-based pricing creates a conflict of interest that's easy to miss until it becomes a problem. When a platform earns a percentage of recovered amounts, the incentive structure tilts toward high-frequency, aggressive outreach -- the kind that can damage customer relationships and push the edges of what's permitted under FDCPA. Your recovery goals and the platform's revenue goals stop being aligned.

Dash uses a fixed monthly platform fee with no commissions and no volume caps. Unlimited accounts, texts, and emails are included. You control outreach intensity, payment plan terms, and communication tone. The platform doesn't benefit from pushing more messages -- so it doesn't. That alignment matters when you're trying to recover payments while keeping a customer relationship intact for future business.

Operational control goes beyond pricing. The ability to configure payment plans, set escalation thresholds, and adjust outreach cadence by account type means your collections strategy reflects your business priorities, not a platform's default settings. See how Dash's platform handles these configurations in a live environment before committing.

Bottom Line: Compliance is not a feature toggle. It is foundational architecture. The right platform enforces rules automatically, logs every interaction, and scales without adding risk to your team or your brand.

Three criteria should drive your selection: system-level compliance controls that run without manual oversight, a pricing model aligned with your recovery goals, and first-party outreach that keeps your brand in direct communication with customers. Platforms that check all three don't just reduce risk -- they give your team the confidence to operate at scale.

Ready to evaluate a platform built for compliant outreach at scale? Request a Dash demo to walk through the compliance workflows firsthand.

Frequently Asked Questions

What makes a collections platform truly FDCPA compliant?

A truly FDCPA compliant collections platform has compliance built into its core architecture, not added later. It automatically enforces rules for contact timing, frequency, and consumer rights at a system level. This includes features like automated contact frequency controls, time zone-aware outreach scheduling, and built-in cease-and-desist handling.

Why is choosing an FDCPA compliant collections platform so critical for businesses today?

Selecting an FDCPA compliant collections platform is critical to reduce regulatory exposure and avoid significant business risks. Without system-level compliance, businesses face potential CFPB enforcement actions, class-action litigation, and reputational damage. With increasing regulatory scrutiny, particularly in sectors like healthcare and financial services, platform selection is a strategic decision for protecting both cash flow and customer relationships.

What specific features should I look for in an FDCPA compliant collections platform?

When evaluating an FDCPA compliant collections platform, prioritize features that provide verifiable protection and control. Look for real-time audit logs of all communication, automated opt-out management, and configurable outreach rules for contact windows and frequency. Additionally, SOC 2 Type 2 certification and support for first-party workflow are key indicators of a platform built to reduce risk.

How does a platform's pricing model impact FDCPA compliant collections?

A platform's pricing model can significantly influence collection practices and compliance. Commission-based pricing might incentivize aggressive outreach, potentially damaging customer relationships and increasing compliance risks. Fixed monthly fees, without commissions or volume caps, allow businesses to maintain control over outreach intensity and communication tone, aligning incentives with compliant, customer-centric recovery.

What is first-party collections and why is it important for FDCPA compliance?

First-party collections mean your business directly communicates with customers regarding overdue payments, rather than outsourcing to a third party. This approach keeps your brand in control of the communication tone and strategy, which is important for FDCPA compliance and preserving customer relationships. By managing collections in-house, businesses can ensure practices align with their values and regulatory requirements.

How does SOC 2 Type 2 certification relate to FDCPA compliant collections platforms?

SOC 2 Type 2 certification provides independent verification that a platform's security and data handling practices meet rigorous enterprise standards. While FDCPA focuses on consumer communication, secure data management is foundational to overall compliance and protecting sensitive customer information. A platform with this certification, like Dash, demonstrates a commitment to maintaining high levels of data integrity and privacy.